November 2020

In October, global stock markets started out strong, gaining 5% through October 12, but then fell 7% over the remainder of the month. Larger-cap U.S. stocks fell 2.7% in the full month (Vanguard 500 Index), while developed international stocks dropped 3.5% (Vanguard FTSE Developed Markets ETF). Emerging-market (EM) stocks were positive in October with a gain of 1.3% (Vanguard FTSE Emerging Markets ETF). Markets were particularly jittery during the last week of October. The S&P 500 fell 5.6% in the final week. The main culprits for the heightened volatility likely included (1) surging COVID-19 cases in the United States and Europe, (2) uncertainty around the election, and (3) Congress’s inability to pass additional fiscal support for the economy in the short term.

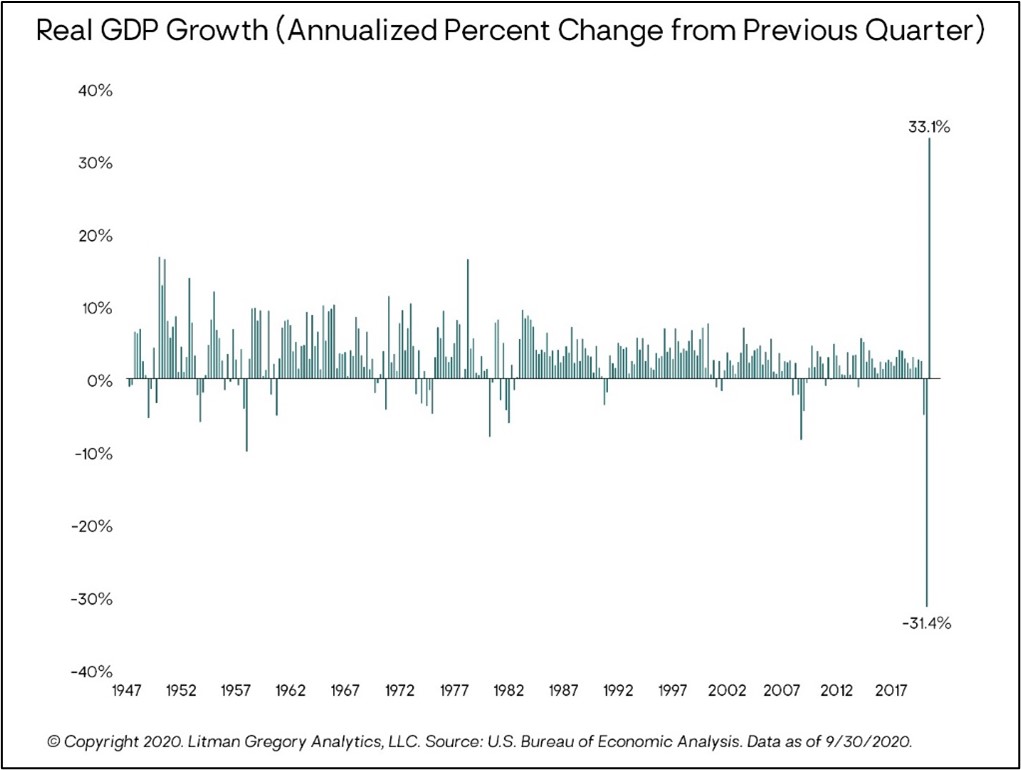

As the U.S. economy opened up over the summer, GDP has sharply rebounded off the lows. The Bureau of Economic Analysis put out their advance estimate for real GDP growth and they pegged it at 33.1% for the third quarter. It was the highest GDP growth rate on record, but it is growth off a low base in the second quarter (which was the worst GDP decline on record). With the sharp ride down and back up, the economy is still 2.9% below where it was one year ago and 3.5% lower than where it started the year. This year’s shutdown and reopening of the economy has thrown off the scale of many economic charts. The readings from 2020 have literally been off the charts. Real GDP growth is just one example (chart below).

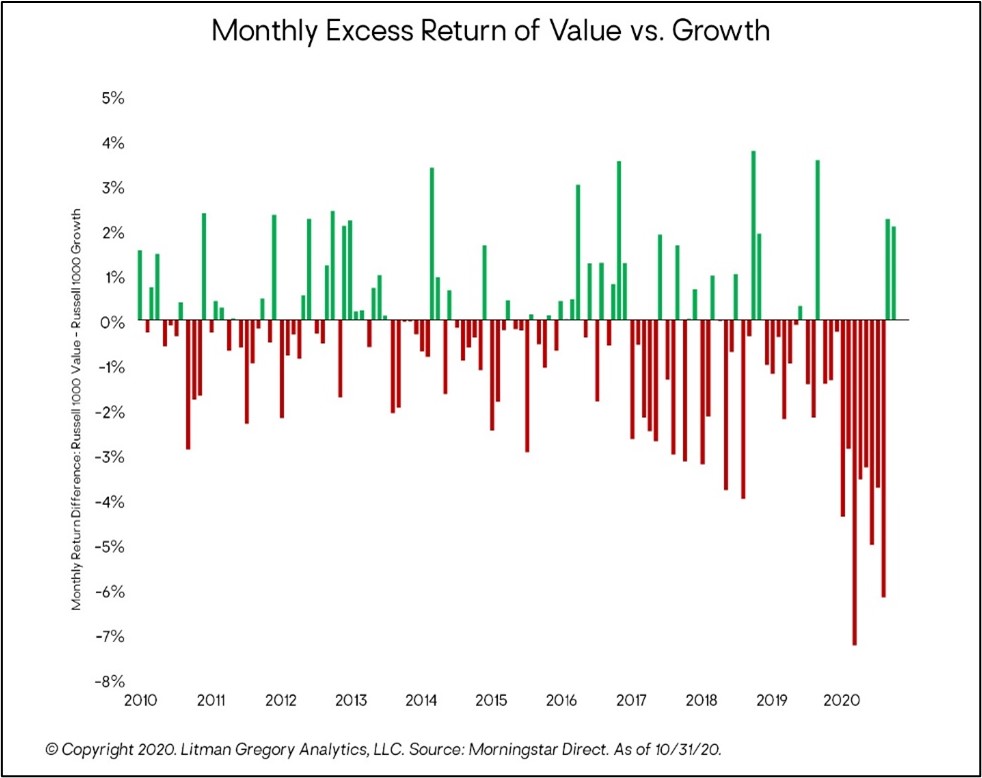

Under the hood, only two S&P 500 sectors were positive last month (utilities and communication services). The technology sector was the worst-performing sector in October with its loss of 5.1%. The underperformance by tech stocks helped fuel value stock’s outperformance relative to growth stocks. The Russell 1000 Value Index outpaced its growth counterpart by more than 2% in October, making it back-to-back months of outperformance. In November, value stocks have a chance to outperform in three consecutive months, something that has not happened since 2016 (see the chart "Monthly Excess Return of Value vs. Growth"). Value investors worldwide can be heard reciting fictional major league baseball manager Lou Brown’s rallying cry: “We won a game yesterday. If we win today, that’s ‘two in a row.’ If we win one tomorrow, that’s called a ‘winning streak.’ It has happened before!” To be fair, value investors are not thinking about a relatively unknown sports comedy from the 90s about the Cleveland Indians. But value stocks are looking to put together a winning streak in November.

Foreign equity markets were mixed during October. Emerging market (EM) stocks outperformed developed-market stocks with a gain of 1.3%. EM Asian stocks helped the most in October. Chinese stocks (MSCI China Index) gained 5.3% and the broader EM Asia region (MSCI EM Asia Index) gained 3.3%. On the whole, that region of the world has so far done a better job navigating the current pandemic. The other main developing regions within the EM index, Europe and Latin America, were negative in October. EM Europe (MSCI EM Europe Index) was the hardest hit with losses of nearly 10%. Many European countries are now dealing with a large second wave of COVID-19. Many developed European economies have re-entered full or partial lockdowns to try to limit the spread of the virus. European equities fell 5.4% in October (Vanguard FTSE Europe ETF), which dragged down the broader foreign developed markets index into negative territory (down 3.5%).

Within the fixed-income markets, the long end of the Treasury curve steepened during the month. The seven-, 10-, 20-, and 30-year rates each increased by about 20 basis points in October. The often quoted 10-year rate finished at 0.88%, up from 0.69% at the start of the month. The steepening yield curve was largely perceived as beginning to price in a “blue wave” sweep for the Democrats in the election. A big win for Democrats is believed to have the potential for more aggressive fiscal stimulus, aid for state and local governments, and infrastructure spending—all of which would require more Treasury issuance in the coming months and years to fund the spending. In October, the gap between five-year Treasury rates and 30-year rates hit its widest gap since 2016.

Higher rates hurt U.S. core bonds during the month leading to 0.6% losses (Vanguard Total Bond Market Index). Treasury bonds fared worse with a loss of 1.4% for the seven- to 10-year maturity portion of the Treasury market. Credit-sensitive areas of the bond market did relatively better due to further credit spread tightening during October. U.S. high-yield bonds and floating-rate loans gained 0.5% and 0.2%, respectively (the ICE BofA U.S. High Yield Cash Pay Index and the S&P/LSTA Leveraged Loan Index, respectively).

As of this writing, we still do not know the outcome of the U.S. presidential election. Election night has come and gone without a clear-cut winner. There is the potential for a drawn-out, contested, and litigated outcome. But we do know that the polls were largely off (again), and the election is much closer than many pundits thought it would be. Morgan Housel recently quoted Nobel laurate Daniel Kahneman’s thoughts on surprises. In a past CFA Institute Annual Conference, Kahneman was quoted saying: “When something happens, you immediately understand how it happens. You immediately have a story and an explanation. You have that sense that you learned something and that you won’t make that mistake again.” However, this conclusion is often wrong. Instead he says, “What you should learn is that you were surprised again. You should learn that the world is more uncertain than you think.”

—Litman Gregory Investment Team (11/5/20)

Certain material in this work is proprietary to and copyrighted by Litman Gregory Analytics and is used by Guardian Financial Partners, LLC with permission. Reproduction or distribution of this material is prohibited and all rights are reserved.